Stablecoins: Where Fiat meets Crypto

In this newsletter, we’re focusing on stablecoins, a key part of DeFi that allows easy participation in decentralized finance. Stablecoins are cryptocurrencies designed to keep their value consistent by being pegged to a stable asset, like fiat money. This feature is what makes them a smart choice for anyone looking to get involved in DeFi with less risk of volatility.

Although I covered them in the context of Infrastructure and Instruments in my book (Chapter 2), they could have easily been a topic of their own. Stablecoins play a significant role in the future of money. As I mentioned in the previous newsletter, I envision the future of money as a competition between stablecoins, CBDCs, and tokenized deposits. However, since central banks are unlikely to take on private sector roles, the real battle is between stablecoins and tokenized deposits. The upcoming SFF features a discussion on this very topic.

Stablecoins can mean many different things

I should also point out here the wide usage of the term stablecoin. I can think of 5 different ‘stablecoins’ who have vastly different properties:

USDC (Regulated)

USDT (Unregulated)

UST (and other algorithmic, unbacked unstablecoins)

Japanese Stablecoins (First G7 nation with stablecoin laws, backed by banks)

Libra (Now history, but significant as precedent and catalyst)

Legislation is starting to catch up by requiring stablecoins to meet minimum standards and disclose relevant information. This is crucial for consumer protection, so that we can avoid another incident like UST. Newcomers may mistakenly assume that all stablecoins are the same at first glance, without realizing the possibility of unexpected collapse for a particular stablecoin.

The price history of a stablecoin is just one factor of stability. Similar to a sheet of ice, failure can occur suddenly and have catastrophic consequences. It is critical to examine the internal composition of a stablecoin and its issuer to assess stability. Without requirements on the issuer by a supervisory body, issuers will have no impetus to disclose internal workings.

You can try it yourself today without being a degen

One exercise I suggest in my book on how people can get started with DeFi is to purchase some USDC (or if you live in Singapore, XSGD). Once you have stablecoins, you can begin exploring the crypto system, using them to pay people and understand the intricacies involved with self-custody. This will involve safekeeping a private key and understanding the distinctions between browser and app-based hot wallets such as Metamask, Trust Wallet, and hardware wallets like Ledger. To become familiar with the system, the best approach is to interact with it directly. Opting for stablecoins instead of volatile cryptoassets not only provides a safer option but also offers the convenience of being able to make payments to individuals and businesses using stablecoins.

Starting from February 2024 when my physical book is out, I will accept XSGD and USDC as payment for my book. When I can physically meet people and sell my book in person, you will be able to pay me with XSGD or USDC, providing a real-world use case.

USDC vs USDT: Comparing the two largest stablecoins

In my book, I covered the business model of stablecoins, how they work, and the major players, such as USDC and USDT. These stablecoins have varying levels of risk. For USDT, regulation is seen as a bug, whereas for USDC, regulation is considered a feature. USDT is often likened to the ultimate eurodollar.

The term "Eurodollar" refers to a dollar that circulates outside the United States. This term has its origins in historical reasons often observed in finance. USDT, being beyond the control of the United States government, offers the advantage of businesses preferring transactions that cannot be censored by the US government. In contrast, USDC has the ability to freeze your assets if required by NYDFS (or other regulator), as stated in its Access Denial Policy.

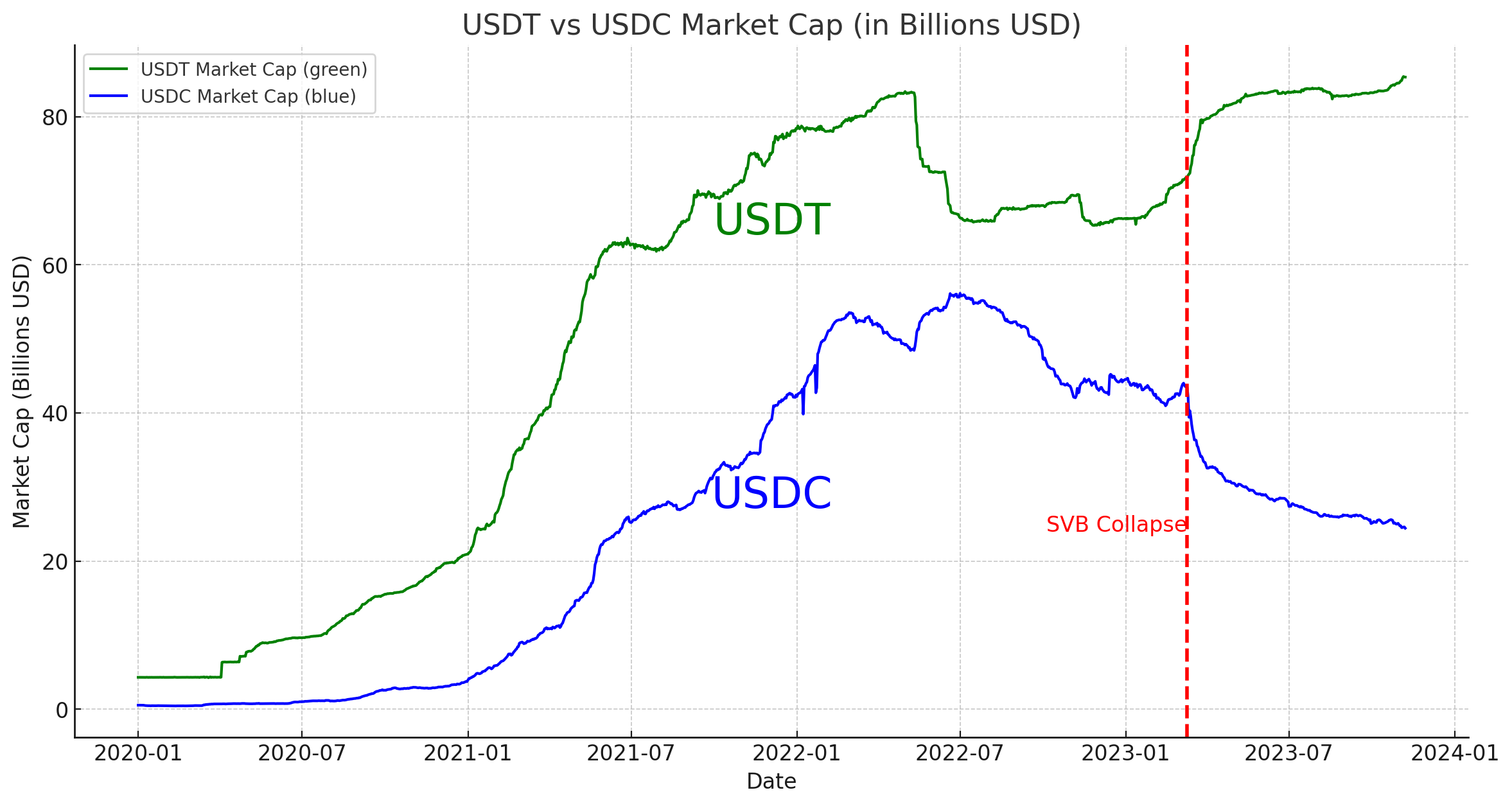

The ill-fated collapse of SVB in March 2023 is the most significant incident in 2023 for stablecoins, causing migration from USDC into USDT. Circle had 8% of collateral in SVB, causing a depeg of USDC to a low of 0.86. It highlighted the interconnectedness of the traditional banking system with stablecoins.

As the diagram illustrates, the circulation of USDT (yes, the unregulated one) has always been higher than USDC. But this became even more so post-SVB. This should tell you somewhat about the motivations behind the users.

Mechanisms

When I was an ETF trader, a common workflow was to create or redeem ETFs. To create ETFs, bring a basket of stocks. Redeeming converts ETFs back into the basket. A similar process exists with stablecoins. When you bring a dollar to Circle to mint USDC, Circle holds the balance and creates a USDC. Conversely, when you bring the USDC back to Circle to redeem your dollar, the USDC is destroyed. This process is straightforward.

Now, the other part of the stablecoin issue is how they generate revenue. Stablecoin issuers do not pay interest on deposits. Circle earns money by investing in fixed income instruments such as treasury bills and other liquid fixed income instruments. The profit is derived from the interest earned on these investments, as well as the interest earned on the collateral used for its float. This is the main profit model for stable coin issuance. There can be other routes to monetisation, via partnerships for example.

Stablecoins vs Tokenized Deposits

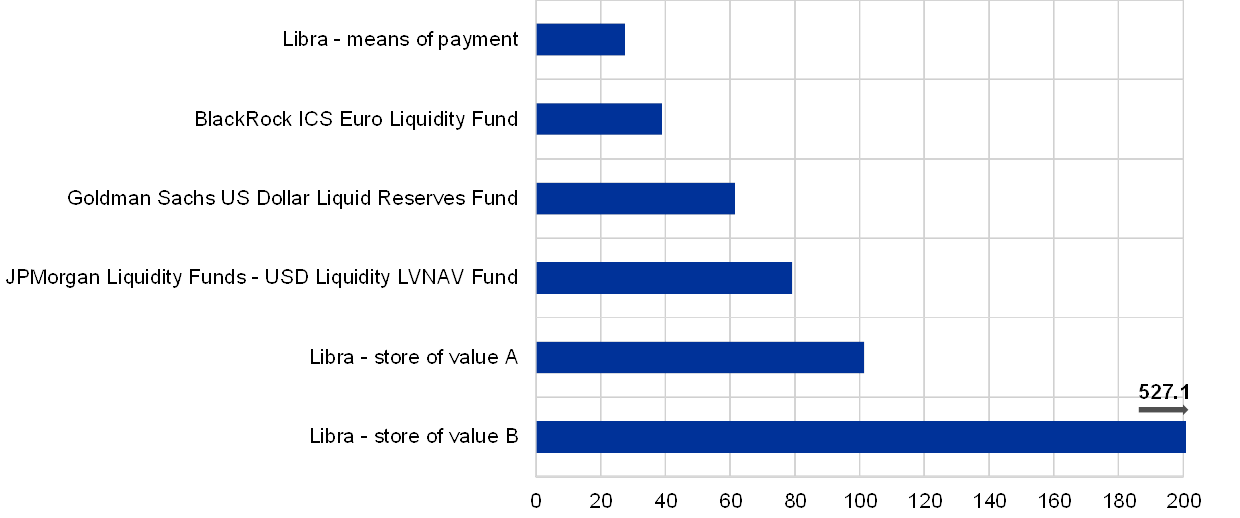

As mentioned in my previous newsletter, the JP Morgan paper raised the topic of collateral. What kind of collateral? These assets must be safe and liquid. By "liquid," we mean that these instruments have deep markets, and can be easily bought and sold without incurring significant spreads. Collectively, they are called High Quality Liquid Assets, HQLA.

This diagram from JPM illustrates the types of HQLA: T-bills, reverse repos, corporate bonds and money market funds (MMFs). It tend goes on to compare the amount of stablecoin reserves invested in the asset, the average daily trading volume of the asset, and the outstanding volume of the asset.

At times of stress (read: panic), there will be large redemptions. This can cause liquidation of HQLA and thus impact the broader markets, possibly causing contagion effects.

This dynamic will be different for each currency. For USD, they are “not yet at a scale to trigger such contagion effects”.

The European Central Bank has studied this issue on stablecoins, taking Libra as an example. They estimated the Libra Reserve had the potential to be one of the largest European MMFs, potentially contributing to the “scarcity of safe assets in the euro area”. As a result, an “outflock shock" affecting the reserve could pose risks to the global and euro area financial markets.

In my previous newsletter, I mentioned that stablecoins operate outside of the fractional reserve model. This point is also emphasized in the BIS paper titled "Stablecoins versus tokenised deposits: implications for the singleness of money" (https://www.bis.org/publ/bisbull73.pdf), which favors tokenized deposits in accordance with the relationship between the central bank and commercial banks.

Nonetheless, I don't think stablecoins are completely done yet. I’m impressed with the speed of innovation that Circle is bringing. Not to mention that stablecoins currently enjoy ‘Metcalfe’s Law’ open network effects. Unlike tokenized deposits, stablecoins already exist and are well-adopted by the crypto community.

When it comes to regulation, Singapore and Japan (and soon HK) have very progressive regulations regarding stablecoins. Japan is the first G7 nation to have certain rules around stablecoin issuance. Mitsubishi UFJ Financial Group (MUFG), the largest financial group in Japan, is currently developing a stablecoin platform called Progmat Coin.

It will be interesting to observe whether Japanese stablecoins will play a significant role in the modern FinTech landscape, with Japan as a case study. Using a stablecoin for cross-border or online transactions is a sensible choice, particularly when considering the significant costs (3%!) associated with credit card payments.

However, the main concern lies in the competition that stablecoins face. Stablecoins are now competing with real-time payment systems, which are essentially free and instant in most developed countries. For instance, in Singapore, we have a fast payment system. So, why would someone choose to use XSGD for payments when SGD is widely accepted?

It will also take time for consumers to understand the difference between the money in their bank account, the money in their FinTech app, and stablecoins. They all carry different counterparty risks (sadly, only understood when SHTF) and different interoperability.

Wrapping up

Other significant effects of stablecoins include those relating to monetary sovereignty of developing countries. For instance, if a citizen in African country can access USD online, without needing to open a bank account, and chooses to hold their wealth in American dollars, it poses a challenge to the monetary sovereignty of the African country.

I haven’t even got to PayPal’s stablecoin yet, which I am still looking into. More to come.

Before I finish, I’d like to mention that there is a chat function on substack. This is a good venue if you would like to connect with me and the community reading this newsletter, and if you’d like to discuss any of the issues covered in the newsletter.

Enjoy your week! Don’t forget to share this newsletter with your colleagues and friends.

Excellent article and insights, looking forward to reading your book. I too am curious about the PYPL stable coin and will be watching for further developments

Excellent thought leadership here, Ken. Lucidly written. Have shared widely.